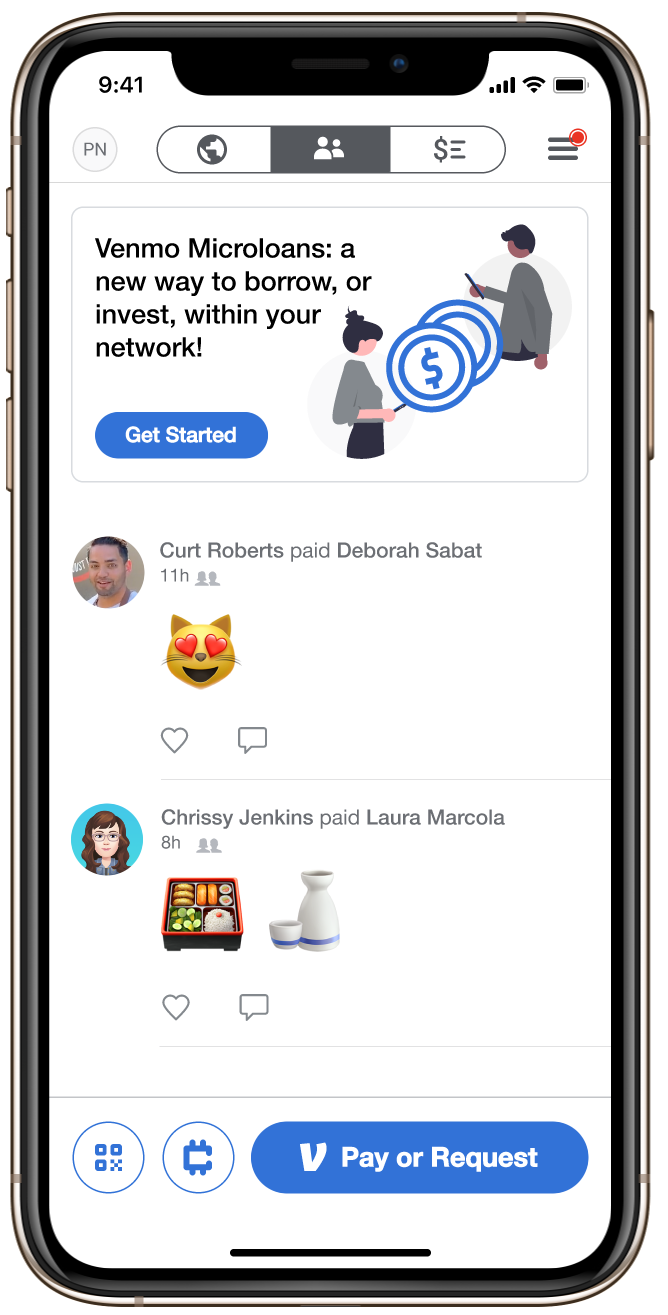

Competitive analysis revealed that Venmo occupies a unique position in the P2P market — it does one thing (payments to friends) very well, and in a way that’s unique and appealing to its audience. Leveraging that appeal of easy financial transactions among friends into a microlending space could create demand for services that typical Venmo users might otherwise avoid, and create a new revenue stream for Venmo through loan interest payments.

While several online platforms already exist that connect lenders to borrowers for microloans, the borrowers are typically impoverished people in underdeveloped countries. No service seemed to exist at the time in the US where friends fund loans to each other in a closed network, earning interest for the friend-lenders.